Filing For Bankruptcy Can Offer An Opportunity To Rebuild Your Life

While declaring bankruptcy does affect your credit score, it also gives you the ability to erase debt and start the process of rebuilding your credit more quickly.

Stop Aggressive Collection Action

Filing for bankruptcy puts a stop to harassing phone calls, repossessions and other aggressive debt collection actions, giving you space to breathe again.

Delay Or Prevent Foreclosure

When you file for Chapter 13 or Chapter 7 bankruptcy, the court issues an order for relief which directs your creditors to stop their collection attempts. This also postpones the foreclosure process, allowing you to keep your house for at least a few more months.

Filing for bankruptcy can sound stressful, but getting started can lift a huge weight from your shoulders.

Finding The Right Solution For Your Unique Needs

There is no minimum debt requirement for filing bankruptcy, meaning almost anyone can do so. However, there are different requirements depending on the chapter you want to file under. Dorothy Bartholomew and our team commonly handle Chapter 7 and Chapter 13 bankruptcy cases.

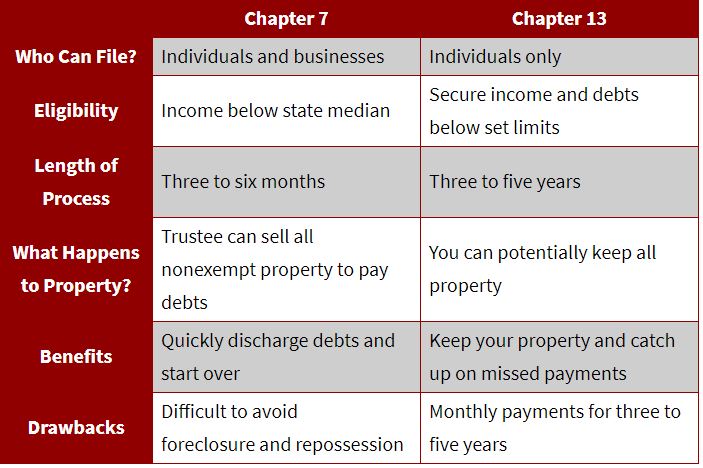

Chapter 7

To determine if you qualify for Chapter 7, the court will look at your average income for the last six months and compare it to the median income for Washington. If you fall below the median, you may choose Chapter 7.

Chapter 13

Also known as a wage earner plan, you can file for Chapter 13 if you have a steady income and you meet the debt requirements set by the U.S. courts.

How do I choose between Chapter 7 and Chapter 13?

The main difference between Chapter 7 and 13 is how your debts are handled. Chapter 7 is considered liquidation bankruptcy, while Chapter 13 is called reorganization bankruptcy.

Get Relief From Crippling Debts With Help From Our Affordable Attorneys

At our debt relief agency, we focus on providing personalized legal services in a stress-free atmosphere. Our Affordable bankruptcy attorneys, Dorothy Bartholomew and Jada Wood, understand what you are going through and can help you every step of the way. Our team has been helping Fife residents rebuild their lives for over 25 years. With over 8,500 past cases and six puppy helpers in our office, you can feel secure in our ability to help you through this difficult and stressful time.

Understanding Chapter 7 Bankruptcy

Chapter 7 bankruptcy is generally the simplest and quickest form of bankruptcy. It is, therefore, the most frequently selected. Chapter 7 is designed for individuals, corporations and partnerships in financial difficulty that lack the ability to pay their existing debts. Under Chapter 7, a trustee is authorized to:

- Take possession of all your nonexempt property

- Liquidate it for cash

- Use the proceeds to pay creditors

If your case is typical of most consumer cases, however, all your assets will be exempt, and the trustee will never take physical possession of any of your property.

How To Get Started

The case is begun by filing the official petition, schedules and a statement of financial affairs. Those forms list all your assets and all your debts, along with some recent financial history. Filing this petition triggers the “automatic stay,” which means your creditors must cease all attempts to collect.

Chapter 7 bankruptcy is generally the simplest and quickest form of bankruptcy.

You must attend one meeting, called a “341 Meeting.” At this meeting, the trustee will place you under oath and can ask you questions about assets and liabilities. The trustee will also give creditors the opportunity to question you on these subjects. But creditors rarely appear at these meetings.

What Happens After The 341 Meeting?

After your “341 meeting,” your only responsibility will be to cooperate with the trustee in providing any information he or she requests. Creditors and the trustee have a 60-day period after the 341 meeting in which to challenge your right to a discharge or the dischargeability of a particular debt. Such actions are relatively rare, which means that in most cases, the court issues a discharge shortly after this 60-day period. Your discharge means that no creditor can hold you personally liable for any debt you owed on the day you filed bankruptcy. It does not, however, prevent a secured creditor from picking up its collateral if you fall behind on the payments. Moreover, there are some exceptions to this broad discharge provision such as:

- Taxes

- Student loans

- Court fines

- Traffic tickets

- DWI damages

- Child or spousal support

If these nondischargeable debts are significant, you might consider filing under Chapter 13.

What Is Chapter 13 Bankruptcy?

A Chapter 13 bankruptcy is useful for those who earn more than the state median income, have assets that they want to keep but would have to give up in Chapter 7, or want to get back a repossessed vehicle. Chapter 13 can:

- Save your home from foreclosure

- Discharge debts that would not otherwise be dischargeable in Chapter 7

- Can reinstate your driver’s license

There are other reasons to file Chapter 13, but those are the most common.

What Happens During A Chapter 13 Bankruptcy?

In a Chapter 13, you will make regular payments to creditors over a period of between three and five years. The size of your payments will depend upon the facts of your case. You need not repay all of your debt.

To qualify for Chapter 13 you must have sufficient income to pay all your necessary monthly living expenses and have some money left over to make Chapter 13 payments.

If you cannot afford to repay all creditors completely, you will propose a plan to pay amounts due on debts that are secured by the collateral (such as your home or vehicles) that you want to keep and other debts that would not be discharged in a Chapter 7, such as:

- Taxes

- Student loans

- Back child support

- Traffic infraction fines

No matter how little you pay to your unsecured creditors, at the end of your plan, your debts will be discharged. Chapter 13 can do many things that Chapter 7 cannot do. But to qualify for Chapter 13, you must have sufficient income to pay all your necessary monthly living expenses and have some money left over to make Chapter 13 payments.

Schedule A Consultation

If you are struggling with debt and want to learn more about filing for bankruptcy, contact our office online or call 253-458-4238 today.